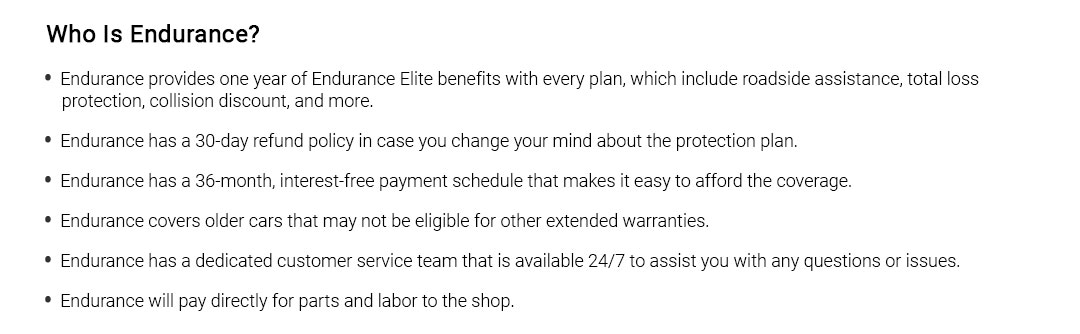

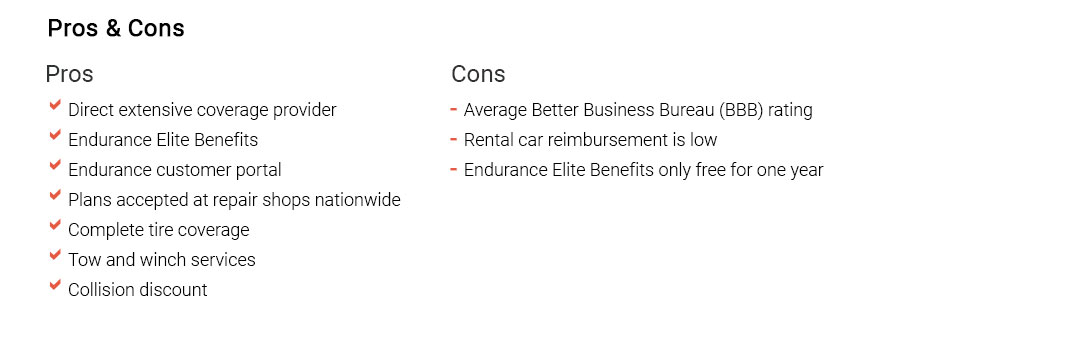

|

|

|

|

|

|

|

|

|

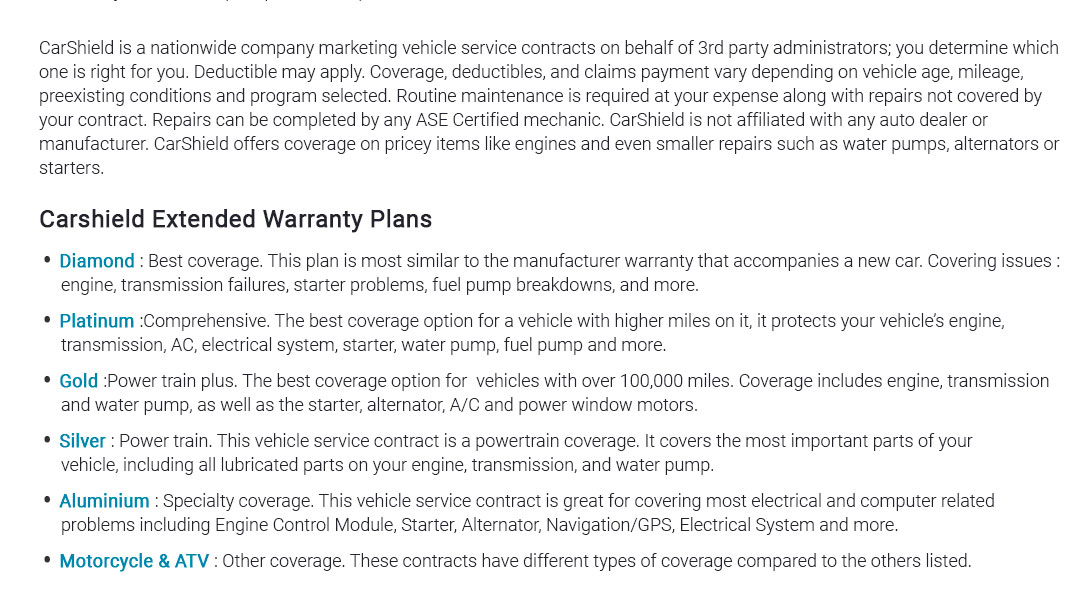

|||

|

|

|

|||||||

|

|||||||

|

|||||||

|

|||||||

|

|||||||

|

|||||||

|

||||||

|

||||||

|

||||||

|

||||||

|

|

|

|

|

|

|

|

mechanical warranty evaluation and value guideWhat it is, plainlyI treat a mechanical warranty as a promise to repair or replace covered mechanical components after a failure, for a set time and mileage or operating hours. It manages risk; it does not remove it. Coverage, in practice

I check the policy's definitions section first; coverage starts and ends with those lines. What it usually won't cover

Expectations I set upfront

Value test: cost vs risk

If the expected outlay without coverage rivals the premium - and volatility is high - I lean toward coverage. If not, I set aside an equivalent reserve. A quiet real-world momentCold Monday, parking lot. The HVAC compressor seized and the belt shredded; the cabin fogged instantly. With the mechanical warranty on file, the shop called for authorization, a reman unit was approved, and I paid a $100 deductible. Rental was covered for two days; I kept the client meeting. Who tends to benefit

Clauses I confirm before signing

How claims typically flow

Reading the tea leavesI finalize by aligning coverage to failure risk, cash flow preference, and service discipline. If the contract is clear, the network is competent, and the numbers pencil out, it earns a yes. If a few gaps remain, I'll keep the offer on the table while I gather one more quote and a sample policy - close, not closed. https://olive.com/

Whether you drive a new vehicle or a used vehicle, olive.com protects your wallet from unexpected auto repair bills. Buy today. Covered tomorrow. https://www.mpp.com/

MPP Company, as a leader in the industry, provides a comprehensive selection of extended warranty services and other automotive protection plans designed to ... https://capstonecoverage.com/the-difference-between-mechanical-breakdown-insurance-and-extended-warranty/

MBI typically covers mechanical and electrical breakdowns, while extended warranties may also include coverage for wear and tear components.

|